A spendthrift clause is a provision in a legal document that stops certain parties from accessing assets before they are distributed to the beneficiary. This can help prevent money from being mismanaged by the beneficiary or seized by a creditor.

This post explains what a spendthrift clause is, how it works and how you can use one.

A spendthrift clause is a condition or requirement that typically appears in legal documents designed to pass on assets, such as wills and trust agreements. The name comes from the word spendthrift — someone who spends their money wastefully. You can use spendthrift clauses as a form of asset protection to can prevent both beneficiaries and creditors from accessing funds before the beneficiary receives them.

For a spendthrift clause to be valid, it must restrain both voluntary and involuntary transfer of a beneficiary's interest. This means the beneficiary can’t use it to get credit and no one else can take it to satisfy a debt. Therefore, spendthrift clauses prevent someone who might not handle money well from wasting it — sort of like a safety net. It also protects the money for all parties involved, such as if there are multiple beneficiaries and one is financially unstable and owes money to creditors.

Spendthrift clauses work by limiting the ability of the beneficiary to sell, give away or misuse the trust's assets, or to use the money as collateral for loans or credit. It also stops the money from being taken by the beneficiary’s creditors if the person is or becomes in debt.

If a trust has a spendthrift clause in it, it’s known as a spendthrift trust.

A life insurance policy can also include a spendthrift clause, giving the insurer the right to protect the funds from creditors. The company may opt to pay the insurance proceeds to the beneficiary in installments rather than one lump sum.

You can use a spendthrift trust to help beneficiaries manage their assets by restricting the amount of money they can access or use for credit (voluntary transfer) and by protecting the funds from their creditors (involuntary transfer). If you’re creating a trust to pass on your assets, you can instruct a trustee (someone appointed to manage the trust) to determine the beneficiary’s financial needs and only release the money they need for living expenses.

Debt collectors usually can't claim the trust's assets directly, like through a lien or court order. However, a creditor may still be able to get a garnishment (a court-ordered collection) on payments to the beneficiary to collect the money. Not all state laws allow for spendthrift trusts, and the rules vary in states that do.

A spendthrift trust typically cannot be broken as it is designed to protect the beneficiary’s inheritance from irresponsible spending habits.

Spendthrift Trust Roles and Responsibilities

A trust agreement typically involves three main roles:

Grantor: Also called a “settlor,” this is the person who transfers the property into a trust.

Beneficiary: This is the person who receives the benefits of the trust, will, or other legal document.

Trustee: This is the person or organization who administers property and other assets according to the terms of the trust.

While some trust documents assign the same person to multiple roles, the beneficiary of a spendthrift trust can never also serve as the trustee. Instead, the trustee will be a different family member, a family friend or even a corporate trustee like a bank.

Some spendthrift trusts give the trustee the authority to stop payouts to a beneficiary who becomes self-destructive, such as in cases of substance abuse. The funds could then accumulate for future payments to the beneficiary, or they could go to another beneficiary entirely. The trustee may also have the option to make payments on behalf of a self-destructive beneficiary while withholding direct cash payouts to the beneficiary.

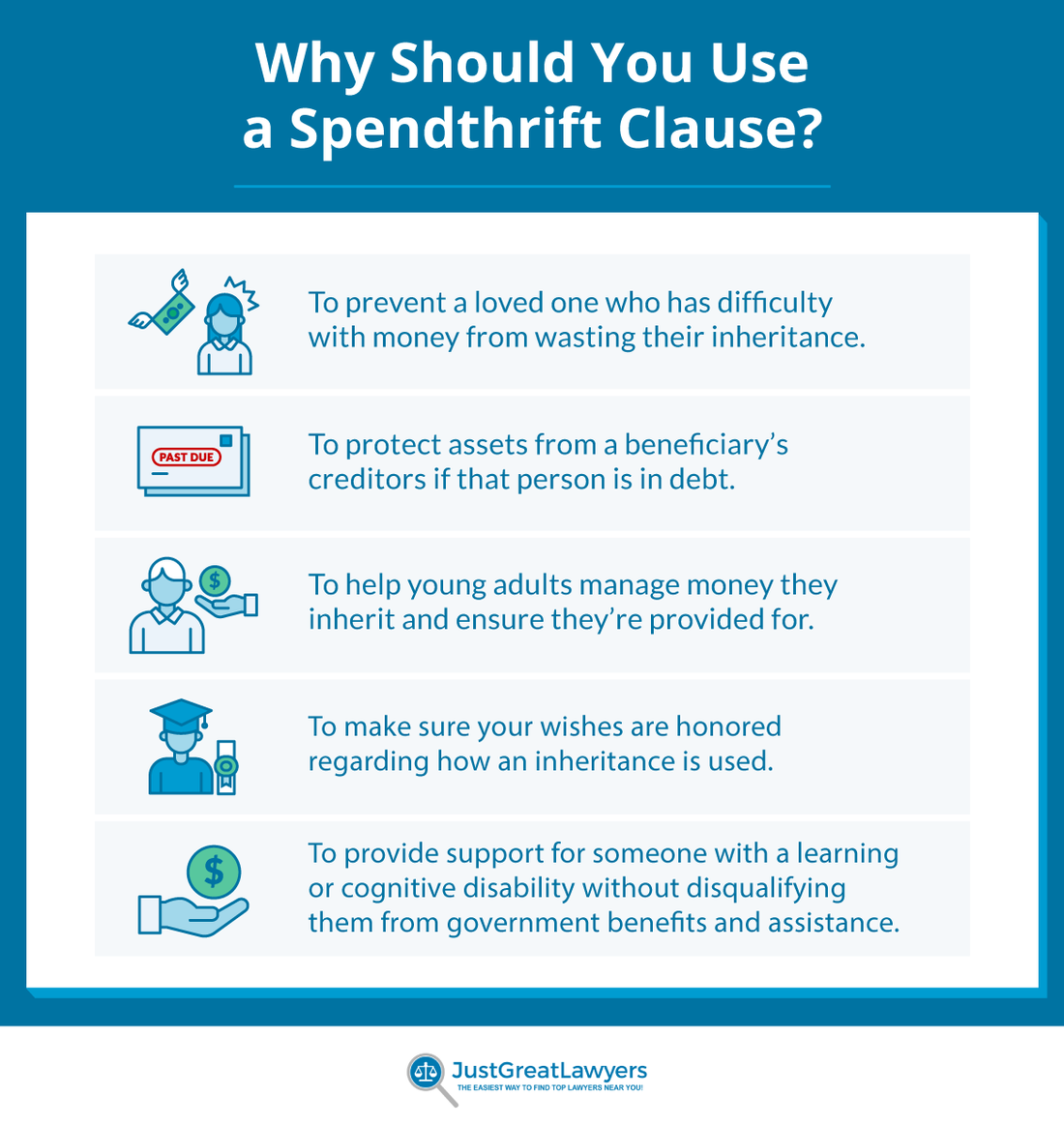

Spendthrift clauses are an essential part of many estate planning tools. Here’s why you may want to include one in yours:

Stop a loved one from wasting their inheritance: Spendthrift trusts may be in the best interests of a beneficiary. If a person has difficulty managing money, a spendthrift clause can help make sure they don’t squander an inheritance.

Protect assets from creditors: Just as the beneficiary can’t access the assets with a spendthrift clause, neither can debt collectors. This protects the inheritance from a creditor's claims unless they garnish the payouts.

Help young people manage money: If the beneficiary is young and not experienced with money, a spendthrift clause can offer peace of mind and help ensure their financial security over time. Spendthrift trusts can also be used to provide an inheritance for grandchildren who are too young for you to know how they will manage their finances.

Ensure your wishes are honored: You may choose to provide for the beneficiary’s living costs only. A spendthrift clause can help ensure that your wishes are honored and that money isn’t used for extravagant purchases.

Care for someone with a learning or cognitive disability: Specific types of spendthrift trusts can help people with a learning or cognitive disability, providing financial support without disqualifying the beneficiary from receiving government benefits and assistance.

The following is an example spendthrift provision in a trust document. Note that it contains clauses specifying the trustee’s role as well as limiting access to assets by both the beneficiary and any creditors.

Article III: Spendthrift Provision

3.1 Nature of Trust: This Trust is and shall be a spendthrift trust under the applicable laws and regulations. No part of the net income or principal shall be liable to be anticipated, pledged, assigned, transferred, or encumbered in any manner, nor shall it be subject to any beneficiary's debts, contracts, obligations, liabilities, or torts.

3.2 Trustee Discretion: The Trustee, [Trustee's Name], has absolute and uncontrolled discretion to determine how much, if any, income or principal from the Trust will be distributed to the beneficiary, [Beneficiary's Name]. The Trustee may take into account the beneficiary's other resources and means of support known to the Trustee.

3.3 Limitations on Transfer: Any attempt by any beneficiary to anticipate, assign, sell, transfer, pledge, encumber, or charge his or her interest in income or principal, whether present or future, is in violation of the express intention of the Grantor and is therefore null and void.

3.4 Protection from Creditors: Neither the principal nor the income of any trust established hereunder shall be subject to attachment or other judicial process by any creditor of any beneficiary. No beneficiary shall have any right or power to anticipate, encumber, or control any part of any income or principal payable to or for the use of such beneficiary, nor shall such income or principal, while in the possession of the Trustee, be liable for, or subject to, the debts, obligations, or liabilities of any such beneficiary.

3.5 Mandatory Exceptions: Notwithstanding the foregoing provisions, the spendthrift protections of this Trust do not apply to obligations imposed by law including but not limited to federal tax liens, alimony, and child support. The Trustee is authorized and instructed to honor any properly presented claim for such obligations.

When would you use such a provision? Say that you want to provide for your son, but worry he won’t handle a large inheritance well due to his troubles managing finances. To prevent this, you set up a spendthrift trust. You designate an estate planning attorney as the trustee who controls the money, providing a set amount to your son each month for living expenses. In addition to preventing your son from squandering all the funds at once, this arrangement protects the trust from your son’s creditors who won’t be able to reach the assets.

Spendthrift trusts can help you provide for loved ones who are young, may be financially irresponsible or have disabilities or substance abuse issues. However, even in this type of trust, the funds aren’t completely untouchable and you’ll want to carefully consider both the advantages and drawbacks to any trust you want to establish.

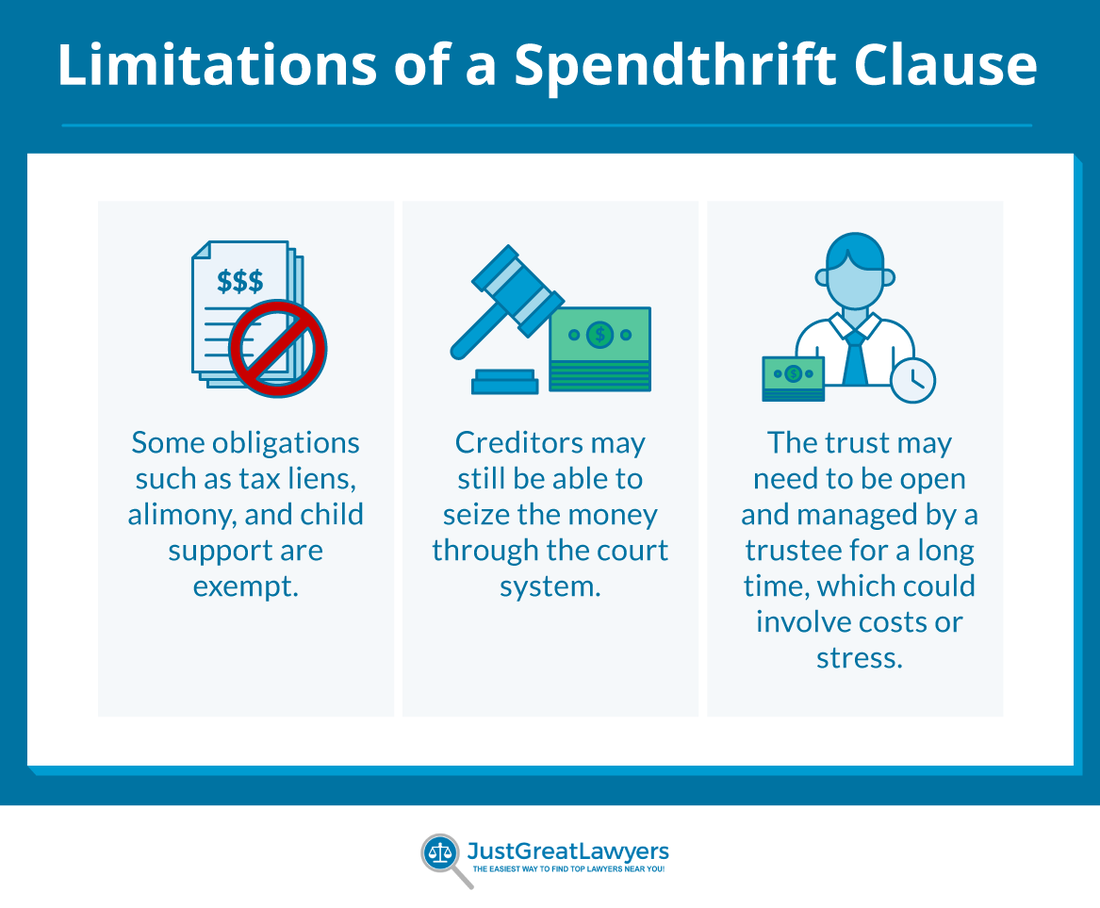

When creating this type of trust, you’ll want to take into account the following limitations and considerations.

Even in spendthrift trusts, certain debts must be paid from trust assets, including the following:

State and federal taxes

Money owed to judgment creditors

Alimony

Child support obligations

Money owed to individuals who provided services to the beneficiary associated with the trust

Debt collectors may still be able to access the assets

If the beneficiary receives more income from the trust than is needed for support, a creditor may be able to reach the assets through the court system.

The trust may remain open for a long time

If you choose to distribute money through periodic payments, your trust may need to stay open for many years. This also means someone would need to manage it for a long period of time. This could involve additional cost if the trustee is a lawyer or stress if it’s a family member or friend.

Whether you want to set up a living trust or provide for family members after you’re gone, an experienced lawyer can help. Just Great Lawyers can instantly connect you with a local attorney who can explain how spendthrift clauses work in your state and how to set up a spendthrift trust if you need one.