Special needs trusts (SNTs) allow beneficiaries to receive an income, while still collecting public disability benefits. In this article, you’ll learn about the types of special needs trusts, how to set up a special needs trust, and what special needs trusts can and can’t be used for.

A special needs trust (sometimes called a supplemental needs trust) is designed to allow individuals with special needs to access additional funds without risking the loss of their government benefits.

Many people with special needs face numerous expenses. At the same time, these individuals also often rely on government benefits such as Medicaid benefits or Supplemental Security Income (SSI).

A special needs trust is one way to allow someone with special needs to maintain a higher quality of life. It gives them access to funds that can be used to pay for various common disability expenses. And, they won’t need to sacrifice their eligibility to receive public benefits.

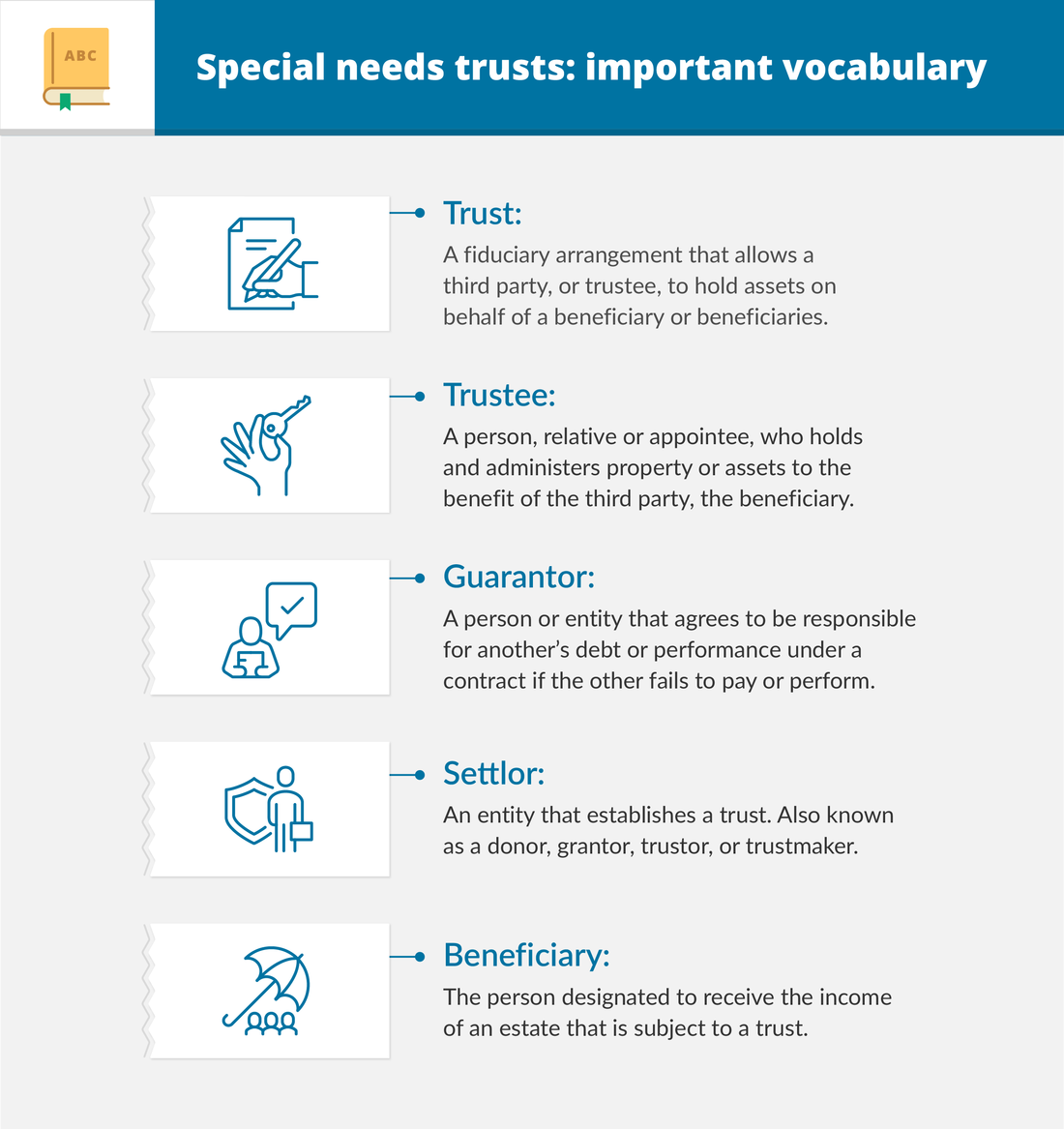

What is a trustee?

The trustee is the person who manages trust assets for the benefit of the beneficiary. The trustee is responsible for approving all expenses coming out of the trust. Trustees owe the beneficiary several legally defined duties, including accounting, compliance, confidentiality, protection, prudence, and more.

SNT trustees must have the beneficiaries’ best interests in mind. Family members are common choices as trustees. However, they must be familiar with the ins and outs of handling a trust, and, specifically, how to navigate the various laws and requirements surrounding trusts and disbursements.

A trustee should also be skilled in handling finances. Often, professionals can assume the role if a family member lacks the appropriate skills to effectively manage a trust. Parents or other close family members remain as co-trustees to advocate for the beneficiary.

Family members can also be trust protectors. While this role does not act as a trustee, it can appoint and remove trustees. And, a trust protector can initiate accounting and investigations on the trust and the trustee.

The beneficiary is the person for whom a trust is established. Typically, a beneficiary with special needs qualifies for Medicaid or Social Security Administration benefits.

However, these programs impose an asset limit and an income limit for each recipient to remain eligible for benefits. Thus, if someone receives a large sum of money, they may lose their benefit eligibility.

Special needs trusts circumvent these limits by supplementing the government benefits. Still, distributions from an SNT are highly regulated. Different government entitlement programs have different requirements for SNTs. Special care must be paid to ensure trust actions don’t violate these requirements. Violations can lead to legal trouble or revoking of government benefits.

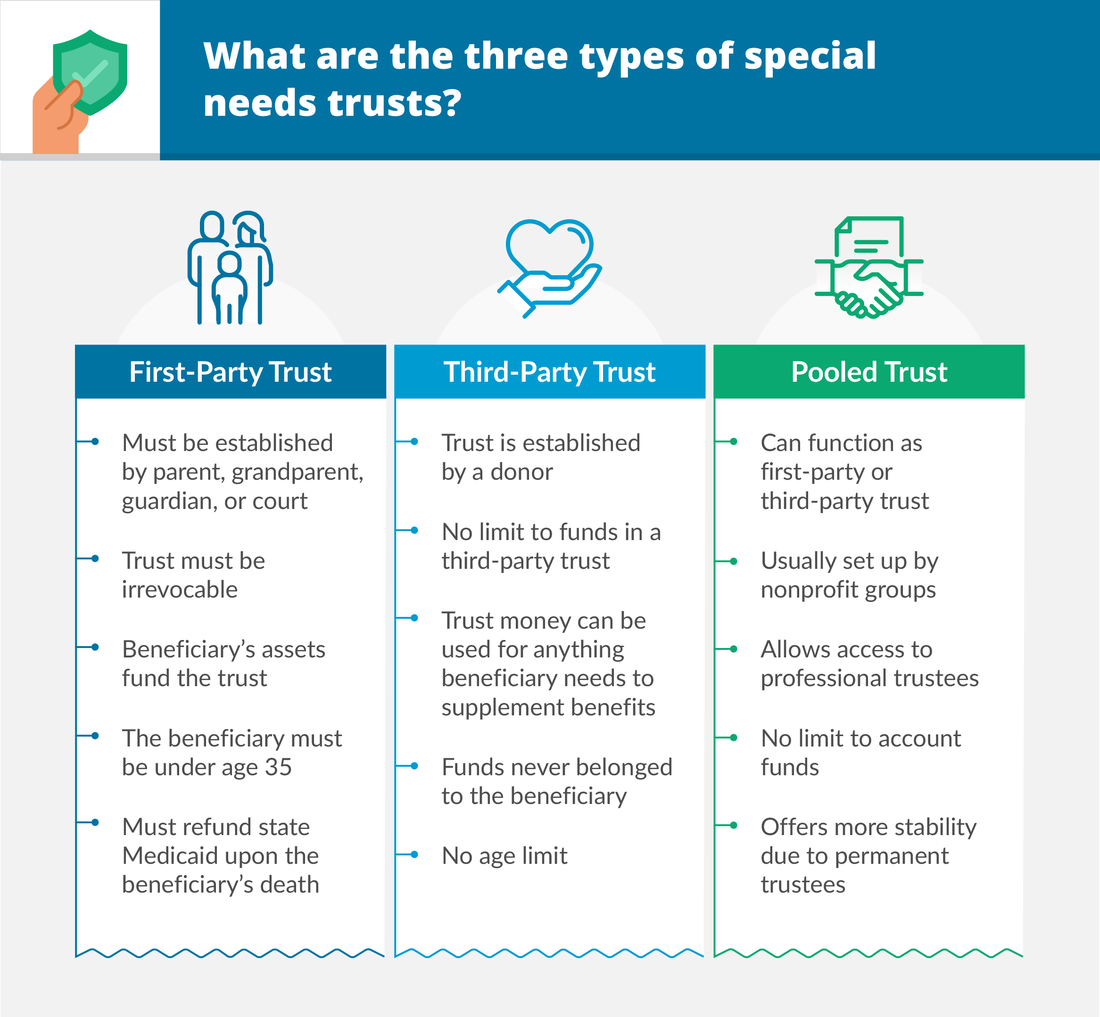

The person who sets up the trust is called the settlor or the grantor. In many cases, the grantor is a parent, grandparent, or sibling of the person with special needs. They may wish for their loved ones to receive assets from them without waiting through the probate process. When any of these parties create the trust, it is called a third-party special needs trust, or third-party SNT.

However, in some instances, an individual with special needs receives a significant amount of money and will open the trust themselves. In this case, the trust is considered a first-party special needs trust.

Pooled trusts can be both first and third-party. As with non-pooled trusts, these are differentiated by who can fund the trust. Third-party pool trusts must be funded with assets that do not, and have never, belonged to the beneficiary.

Special needs trusts allow beneficiaries to receive additional income separate from government assistance.

In some cases, an individual with special needs will come into a significant amount of money and set up the trust themselves. For example, someone may receive an inheritance, settle a personal injury case, or receive the proceeds from a life insurance policy.

When a grantor sets up a trust, they name a trustee who oversees the distribution of trust assets. The trustee should have both a knowledge of the governing laws and a good relationship with the beneficiary.

When the beneficiary wants to make a qualified purchase, they request that the trustee use trust assets. The trustee then considers the request and determines if it is an eligible expense. If so, the trustee uses trust assets to pay for the item or service.

Trustees generally should not distribute cash directly to the trustee. This may count as “income” for the purposes of reporting to government programs.

First-party trusts are funded by assets belonging to the beneficiary. These trusts function in the same way. They provide funds for expenses not covered by government assistance. Since 2016, competent beneficiaries have been able to fund their own trusts.

These trusts are typically used in two scenarios. First, when an individual with special needs has existing assets and knows that they will one day require public benefits, first-party SNTs allow them to set aside their assets into a trust. When the beneficiary starts receiving benefits, the trust is used to fund other expenses.

The second scenario is when a person with special needs receives a large sum of money. Inheritance, lawsuit settlements, and even divorce settlements can count as income. This can disqualify someone from receiving SSI and other benefits. Placing these assets in a trust allows government benefits to continue.

First-party trusts have specific stipulations. They can only be established by individuals under the age of 65. Also, at the time of the beneficiary’s death, all received Medicaid benefits must be repaid in full. This can often drain the trust of its remaining funds.

A third-party trust is created and funded by anyone other than the beneficiary. They are usually established by parents. The funds’ use must abide by the requirements of government assistance programs. Because of this, trust funds are typically used for uncovered medical expenses, caretaker payments, and other allowable expenses. SSI covers food and shelter expenses.

Third-party SNTs are also protected from the beneficiary’s creditors. And, the funds pass back to the trustees in the event of the beneficiary’s death. Third-party SNTs are not required to pay back Medicaid expenses. Also, beneficiaries have no control over the disbursement of trust funds.

Pooled SNTs are different from other trust types. Run by non-profit organizations, these trusts combine the funds of many beneficiaries into one “pooled” account. Individual beneficiaries maintain subaccounts, which are further funded from the total earnings of the pooled resources. Both first and third-party pooled trusts can be created.

Though pooled trusts are less common, they are attractive options for certain situations. Because of the complex legal and financial requirements, SNTs require adept knowledge and capabilities. Pooled trusts are run by financial experts and professional trustees. These nonprofits often partner with other financial institutions to handle investments.

Pooled trusts are typically more financially stable. The nonprofits have a visible history of returns and success. And, the pooling of funds allows greater investment diversification.

Setting up a special needs trust is an involved financial process. Technically, there is no minimum amount required to open an SNT.

Trust funding amounts will vary from situation to situation. There is no mandated minimum for funding, but all trusts cost money to establish and run. These costs can start around $2,000. However, prices will rise with higher fund amounts and complexity. Professional trustees also charge yearly fees, typically between 0.5% to 1.5%. Because of these factors, most experts recommend funding trusts with at least $100,000.

Initial funding must also consider all of the beneficiary’s potentially needed expenses. Medicaid, SSI, and other government benefits can cover specific expenses, including most medical payments and food purchases. Additional expenses can include education costs, transportation, and clothing. Yearly administration fees and trustee payments must also be accounted for.

Third-party trusts should include room for inflation over the expected remaining life of the beneficiary. This is especially true if the trustees will most likely pass before the beneficiary.

Determining what kind of trust to set up depends on the beneficiary.

First-party trusts are best when an individual had assets before becoming disabled, or for those who have received funds while qualifying for assistance. These trusts are advised for individuals who still have the mental faculties needed for money management.

Third-party trusts are the most common type of SNT. These are best when potential beneficiaries can’t make financial decisions for themselves. Typically, these trusts are established by parents for their children. Third-party trusts do not have to pay back Medicaid or other government expenses. However, third-party trusts don’t allow for much (if any) input from the beneficiary.

Pooled trusts allow individuals with more limited assets to benefit from a trust. As these funds are pooled, there are greater investment opportunities to provide better returns. Based on federal law, having more than $2,000 in assets often disqualifies someone from receiving government benefits. Pooled trusts help bridge the gap between too much and not enough.

Deciding on a trustee is a pivotal component of starting a special needs trust. A trustee must be trustworthy and financially intelligent. They must also have the beneficiary’s security at the front of their mind. Third-party trustees are often parents. They are typically best qualified to determine the beneficiary’s wishes. However, as trusts are complex legal and financial accounts, professionals are often chosen or consulted.

Professional trustees are selected when the parents (or others) know they won’t have the means to manage the trust properly. Professional trustees also have the financial and legal knowledge of trust specifics. Parents can remain involved with the trust, either as advisors or co-trustees. No matter the trustee, letters of intent should be written. These describe the needs and preferences of the beneficiary, as well as any financial goals or future support needs.

Because of the heavy toll that comes with managing a trust, professionals are often employed to assist with managing the trust.

Trust documents legally state the purpose and intentions of the trust. These are in-depth legal documents that require explicit details. They must state what the funds will be used for, who the trustees are, and their discretion over disbursements. The document must indicate tax and repayment duties. It should list requirements for successor trustees. And, it should give explicit directions for after the beneficiary has passed away.

Anyone can make these documents. There are abundant legal guides to help decide how and when to write a trust document. There are free templates online. And, there are several tools that allow information to be entered to return a completed document. As with any legal document, consulting an attorney or grant professional is often pertinent.

Professionals are specialized in trust documents. They also have connections with other professionals who focus on special needs trusts. This can include attorneys and financial planners. Having someone who knows every law and requirement is an excellent idea when starting a trust, even in an advisory role.

An invaluable tool to provide funds to people with special needs.

The initial funds are tax-deductible, and they are protected from creditors.

The money is only available for the well-being of the beneficiary.

They allow caretakers to ensure the long-term care of the beneficiary.

They often have high initial and yearly maintenance costs.

Upon death of the beneficiary, first-party SNTs are required to pay back all Medicaid and SSI services. This usually empties the trust, leaving nothing for any named beneficiaries.

Third-party SNTs are exempt from repaying Medicaid and SSI. However, the beneficiary has little control over the trust itself.

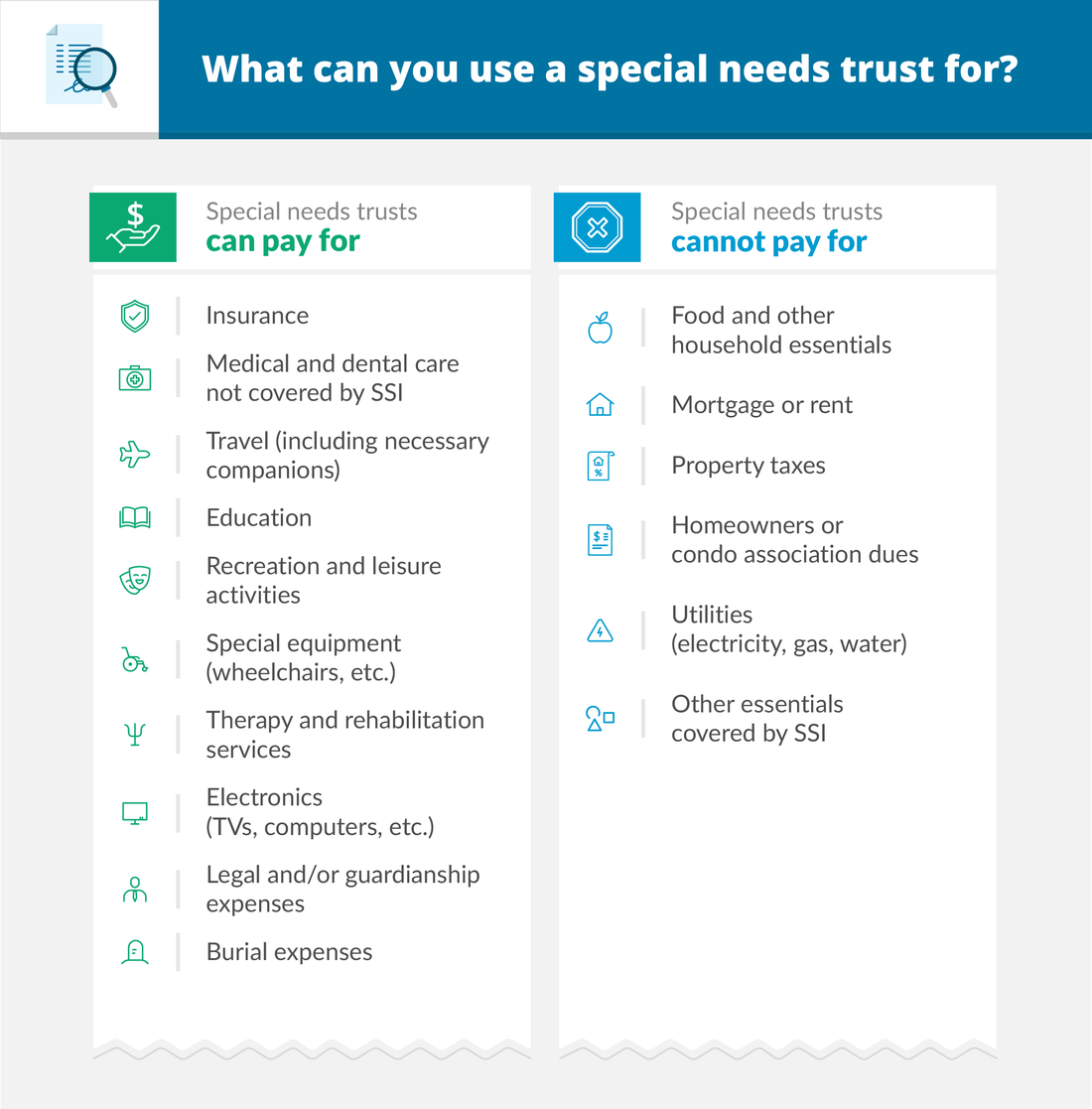

Trust funds are used for daily expenses not related to assisted food and shelter. This includes medical costs outside of Medicaid and Medicare, such as some therapies, dental care, and service animals. These funds also cover specialized medical equipment such as wheelchairs, rehabilitation items, and customized special needs vehicles.

Other common expenses include travel and recreation, as well as computers and phones. These funds are also used to pay for the trust itself. All trustees, even family members, are paid for their services. Payments to spouses and family can also be set up. Other financial requirements, including insurance, legal fees, and end-of-life expenses, can be paid using trust funds.

Trust funds are designed to supplement government assistance. As such, they can’t pay for food, housing, and medical expenses covered under government assistance. The trust can’t disburse cash directly to the beneficiary—all expenses must be paid by the trust.

Specifically, a special needs trust will not cover:

Food and groceries (including restaurants)

Rent or mortgage

Property taxes

Homeowners Association (HOA) fees

House insurance (if required by a mortgage)

Utilities and hookup charges

Trusts are established so that beneficiaries can receive government benefits alongside private funds. Having a high personal value can exclude a person with special needs from government benefits. If an expense is covered by government assistance, it will typically not be eligible for trust funds.

If you have a loved one with special needs and the means to provide them with additional support, an estate planning attorney may be a good option. While the concept is relatively straightforward, the nuances that go into properly setting up a special needs trust are quite complex. Estate planning attorneys can navigate the legality, and they can assist families in setting up personalized financial futures.

For example, opening an ABLE account may be a good idea to give the beneficiary additional control over their own finances. Often, the best approach is to consider an individual’s entire needs and create a comprehensive plan to take care of everything, rather than approaching it piecemeal.

These are not decisions to make if you’re underinformed. Those considering creating a special needs trust should consult an experienced special needs or elder law attorney to ensure that the trust complies with all legal requirements.

Many estate planning and elder law attorneys offer a free consultation, during which they can answer all of your preliminary questions. As a side benefit, they generally can answer other elder law or estate planning questions. They can also give you an estimate of the total cost for creating the trust.